Representing

Accident Victims

Throughout Florida

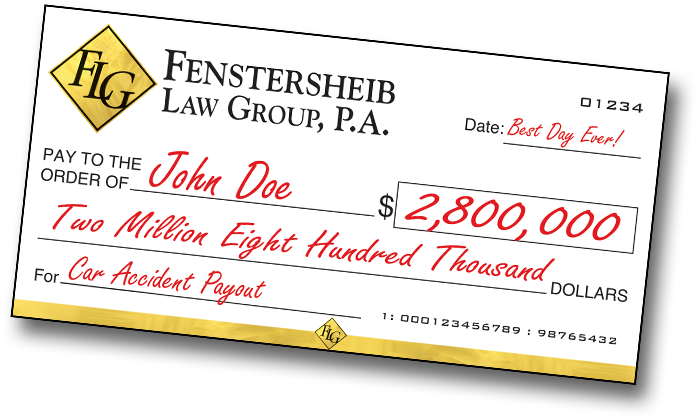

When experience matters, Fenstersheib Law Group has been fighting on behalf of accident victims since 1985 and has recovered more than $500,000,000 for our clients.

Accidents happen and are completely unexpected. If you or a loved one has suffered an injury caused in an accident which was someone else’s fault, you might be entitled to reimbursement. However, you have to be careful of insurance agents trying to settle your claim. Rarely are these ever fair, and if you accept the offer, there is nothing you can do later on to get the justice and compensation you deserve.

At Fenstersheib Law Group, P.A., we are advocates for you and your injury, we are ready to help people (just like YOU) who would otherwise have no legal voice. We feel your pain and along with our legal experience, we offer understanding and compassion. READ MORE

EVENTSLanguages Spoken: English, Spanish, Russian, French and Creole

Robert David

Fenstersheib, Esq.

Stephanie

Fenstersheib, Esq.